Executives are more hopeful about the economy—and their own companies’ performance—than they have been since the COVID-19 crisis began.

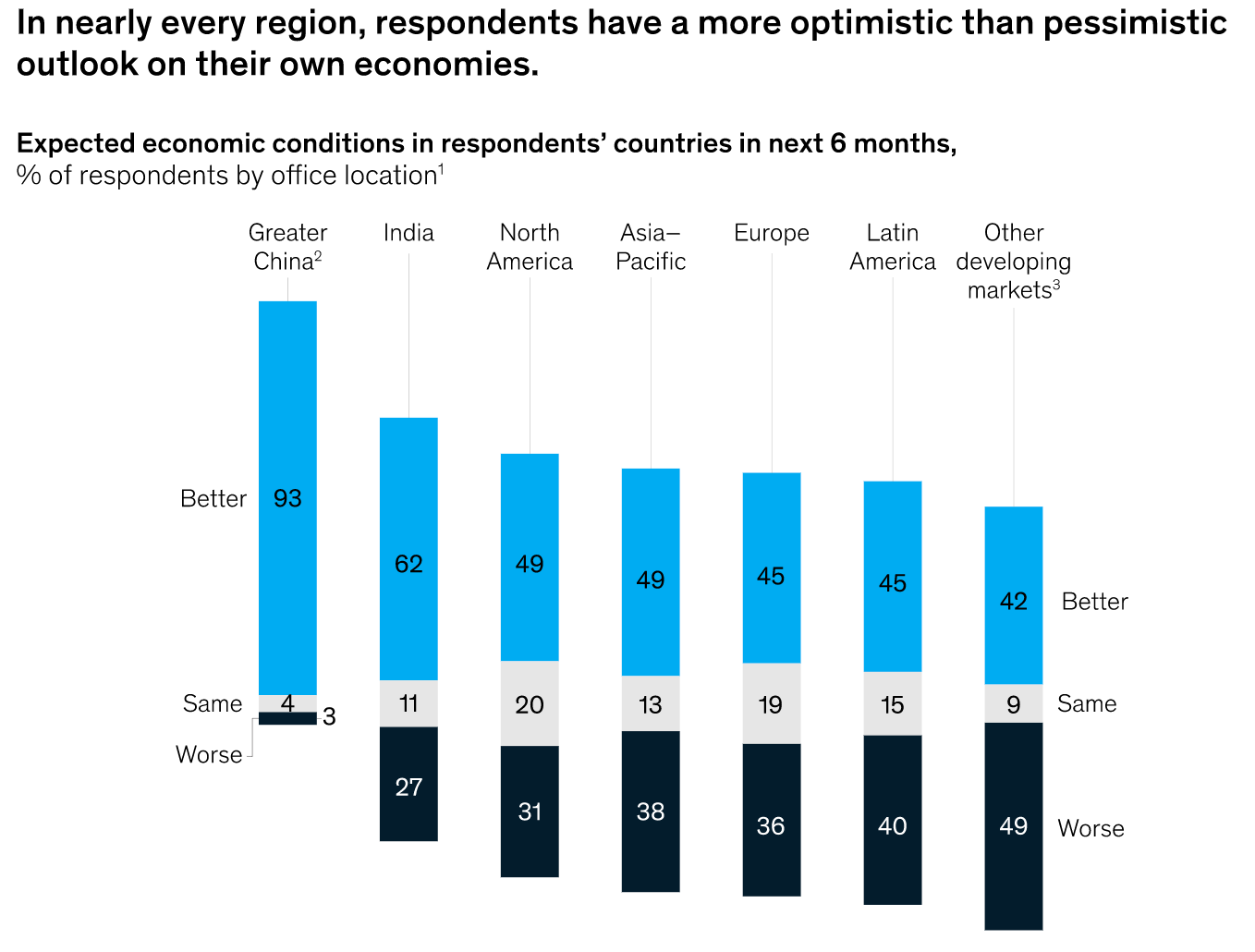

Six months after WHO declared COVID-19 to be a global pandemic, the responses to our latest McKinsey Global Survey suggest a positive shift in economic sentiment. More than half of all executives surveyed say economic conditions in their own countries will be better six months from now, while another 30 percent say they will worsen: it’s the smallest share of respondents all year to expect declining conditions. And except for those in developing markets, respondents in every region are more likely to predict that conditions will improve than that conditions will worsen. That is even true of those in North America, where, between June and July 2020, respondents’ outlooks had taken a negative turn.

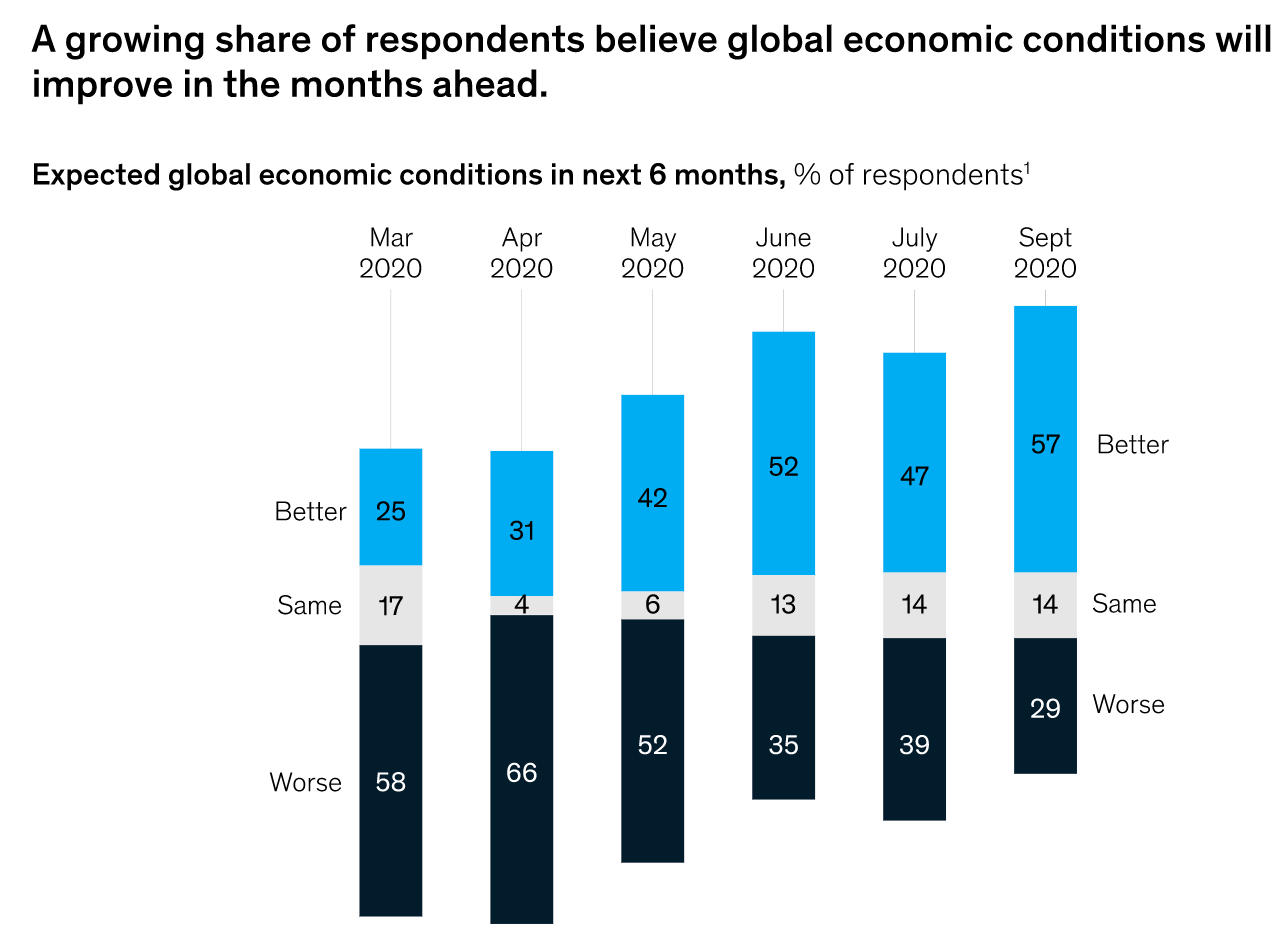

The share of respondents predicting improvements in the global economy has also grown over the past few months (Exhibit 2). Now 57 percent say so, compared with 52 percent in June and 25 percent in March. Across regions, emerging-economy respondents report more positive views on the global economy than their peers do: 73 percent expect global conditions to improve in the next six months, compared with 49 percent in developed economies—a much greater gap than previous surveys this year.

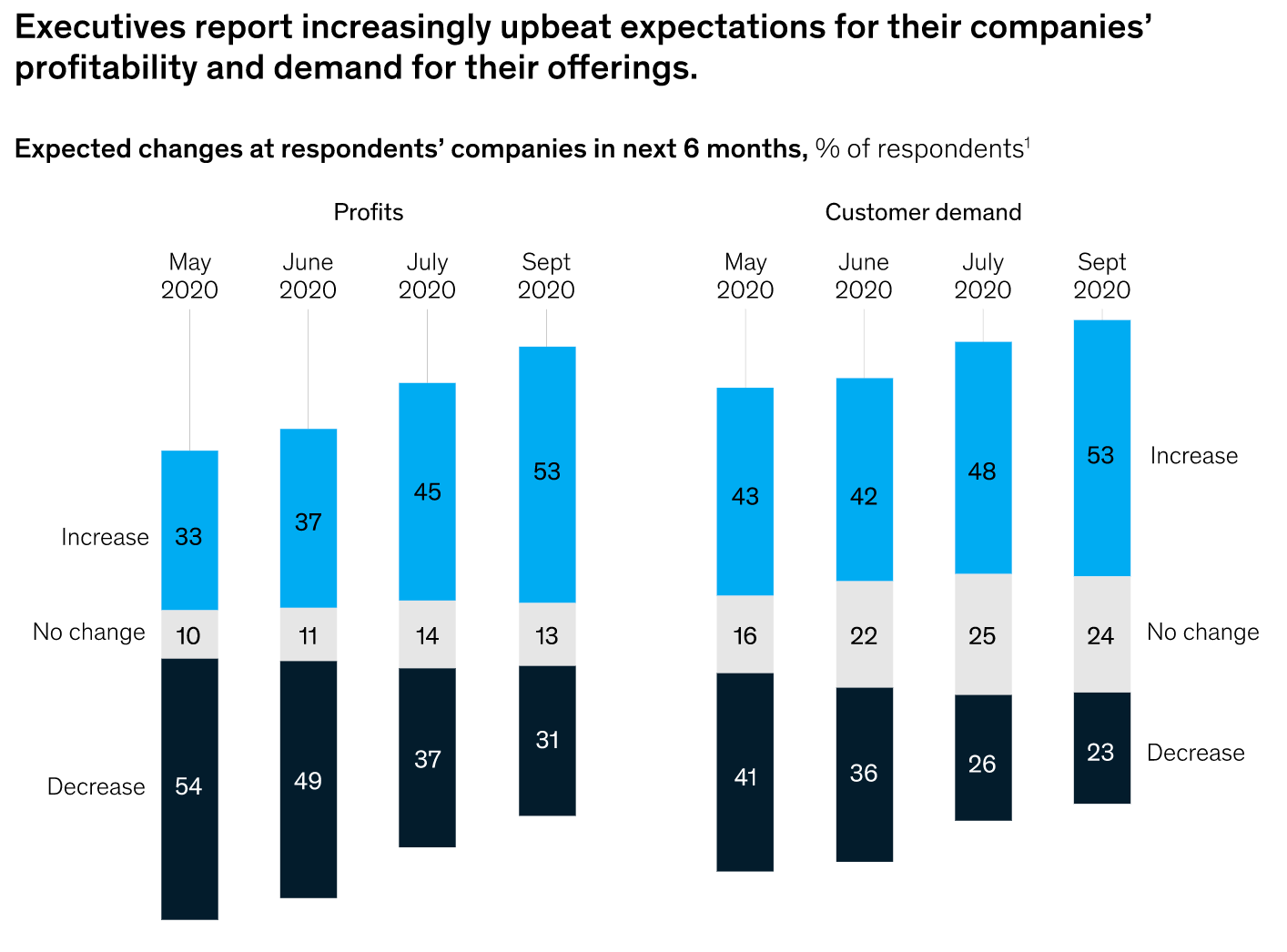

Likewise, hopes are increasingly high for respondents’ own companies. For the first time in 2020, majorities predict that both demand and profits will increase in the months ahead.

The survey results also suggest shifting views about the COVID-19 pandemic’s impact on GDP, at least close to home. When asked which of the nine pandemic-related scenarios is most likely, respondents continue to pick the same scenario for the global economy as they have since the spring: A1, characterized by partially effective policy and public-health responses and a years-long economic recovery. But for respondents’ own economies, executives now select a scenario that involves virus containment, sector damage, and a lower growth rate over the long term (B1) most often.

For more detail on the survey’s results, please see our longer article, “Economic Conditions Snapshot, September 2020: McKinsey Global Survey results.”

By McKinsey & Company