The Reserve Bank decided to keep interest rates on hold at 4.1% because it thinks there’s a chance – just a chance – it has lifted them all it needs to.

In his statement released after Tuesday’s board meeting, Governor Philip Lowe said while inflation was still too high and set to remain so for some time yet, it had “passed its peak”.

Growth in the Australian economy had slowed and labour market conditions had eased, although they remained tight.

After 12 near-consecutive rate hikes, and in light of the “uncertainty surrounding the economic outlook”, it had decided to wait at least a month before hiking again until it knew more about the impact of what it has done on inflation and the health of the economy.

And when you compare Australians’ experience of rising rates with other countries, the Reserve Bank has already done more than many people realise.

Rising rates have hit Australian borrowers harder

Criticism of Australia’s Reserve Bank for not pushing up its cash rate as far as other countries overlooks an important difference between Australian borrowers and borrowers in those countries.

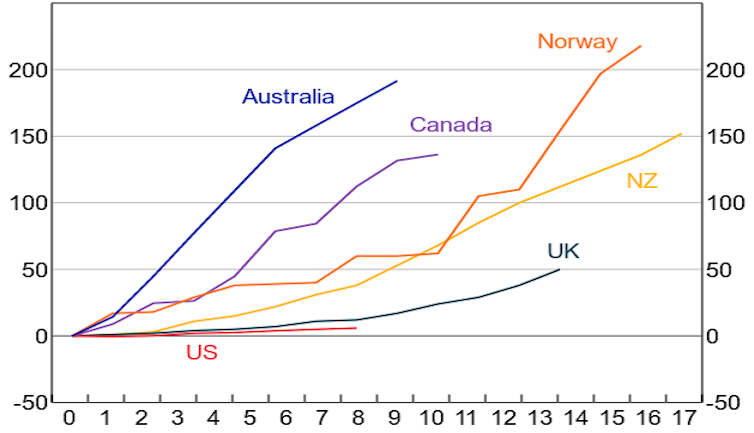

Canada has lifted its central bank rate from close to zero to 4.75%, Britain to 5%, the US to just above 5% and New Zealand to 5.5%.

Yet Australia’s increase – from close to zero to 4.1% – has caused Australian borrowers much, much more pain than borrowers in those other countries.

That’s because an exceptionally large proportion of Australian mortgage holders are on variable rates: roughly 70%. That’s compared to 35% in Canada, 15% in the UK, 12% in New Zealand and less than 5% in the United States.

In the words of Australia’s Reserve Bank: “interest rates on loans with very long fixed-rate terms tend to be less sensitive to changes in the short-term rates”.

Back in February, the Reserve Bank’s estimate was that the interest rates actually paid on Australian mortgages had climbed two percentage points since it began pushing up rates.

In contrast – as this Reserve Bank chart shows – the rates actually paid in New Zealand had climbed by one and half percentage points, the rates in the UK by just half a percentage point, and the rates in the United States by very little at all.

Increases in mortgage rates actually paid

Months since the official rate began climbing. 100 = one percentage point

And because mortgages themselves are so much bigger than they used to be, the dramatic increase in rates actually paid costs a lot more than it would have.

Modelling by Ben Phillips at the ANU’s Centre for Social Research and Methods suggests that in the past two years, the average share of mortgaged households’ post-tax income devoted to payments has jumped from 17% to 25% – the biggest share in an awfully long time.

And it’s set to get worse, whatever the bank does to its cash rate.

The looming mortgage cliff

Usually, Australians take out very few fixed-rate mortgages. But in 2020 and 2021, we took out lots with fixed two- and three-year rates, when fixed rates were low.

As many as 880,000 of those fixed-rate terms are about to expire, pushing those borrowers from rates of around 2% (which might cost $2,100 per month to service) to rates nearer 5.5% (which might cost $3,000 to service).

The Reserve Bank itself expects 15% of borrowers to find themselves with negative cash flows in the coming months – meaning their incomings won’t match their outgoings and they’ll have to run down savings, work more hours, or tighten belts.

We’re already winding back spending. Although total retail spending has climbed 4.2% over the past year, prices have probably climbed 7% while the population has climbed 2%. This means the amount bought per person has shrunk sharply.

Recession is increasingly likely

Anything that makes us cut back even more runs the risk of bringing on a recession, something that’s already happened in New Zealand and may be about to happen in the United Kingdom.

At the start of this week, The Conversation’s expert forecasting panel assigned a 38% probability to a recession in Australia, much more than at the start of the year, but still less than 50% – meaning we might escape it.

The panel’s central forecast is for two more rate hikes this year, which it expects to be quickly unwound. If that happens, and if we escape a recession, the panel expects unemployment to climb only modestly over the year ahead while inflation glides down to 3.9% – within spitting distance of the Reserve Bank’s 2-3% target.

Lowe says getting things right means staying on a narrow path.

The case for living with higher inflation

That path might mean accepting a slower glide down in inflation than some would like, or even a higher end point – something closer to 3% than 2-3%.

Nobel prize-winning economist Paul Krugman this week suggested quietly abandoning the US inflation target (of 2%) once inflation dropped to a point where people no longer noticed it all the time, which he thought would be about 3-4%.

There would be a case for doing that here, so long as inflation was stable, predictable and no longer causing alarm. It’d help keep unemployment low.

In any event, we’re nowhere near there yet. The March quarter inflation figure (the most recent quarterly figure) put the annual rate at 7%. The update due in three weeks will show how quickly we are moving toward 4%.

When we get there, Lowe or his successor (Lowe’s term expires in September) will have time to think about how important ultra-low inflation of 2-3% really is, and whether it is worth the cost to Australians of getting there.

Source: The Conversation